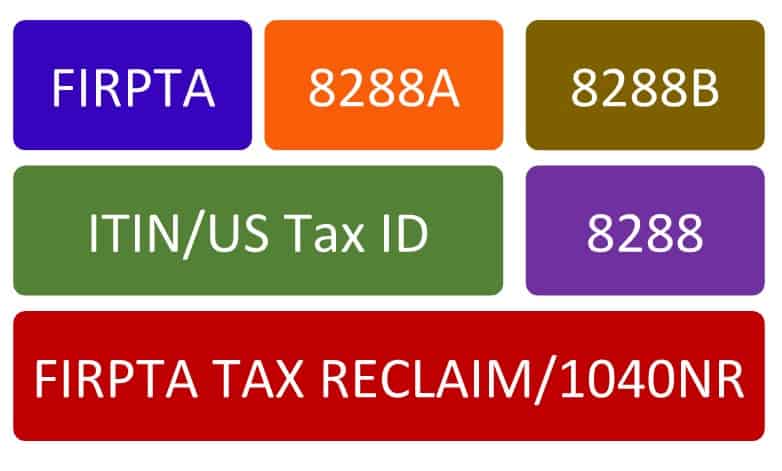

What is FIRPTA?

When any foreign person sells is USA-based property, they are subject to the FIRPTA TAX withholding as per the (Foreign Investment in Real Property Tax Act) at the rate of 10% or 15% of the Gross Proceeds by the US Escrow/Selling agent. For example: Sale price of the US property sale value is $100,000×15% = $15,000. If US Property sale value is $400,000 X10%=$40,000 [if conditions not met please below on 8288B section].

Can I avoid the FIRPTA Tax?

Yes, Provided the seller of the property has a valid ITIN/US Tax ID or apply for ITIN [For more information on ITIN click here ITIN] and start the process to apply for exemption 3 to 4 months advance before the date of closing by completing the Form 8288B. We say the time frame of 3 to 4 months in advance because the processing time is a minimum of 90 days for exemption approval. From our experience with the COVID pandemic situation, there have been significant processing delays estimated at 6 to 9 months.

Who is eligible for FIRPTA Tax exemption with completion of Form 8288–B [Withholding Certificate for Dispositions by Foreign Persons]?

For withholding exemption certification claim, these conditions apply :

- Property sale proceeds value is below $300,000.

- The expected profit or capital gains to be less than or equal to $40,000 per person.

- If Jointly held property – 50% split and reporting recommended to qualify for threshold [Tax planning tip]

If the US property seller meets these conditions, and the IRS issues exemption approval, no FIRPTA tax withholding is required. If not, a minimum of 10% of the sale value to be withheld by the US Escrow team; this is mandatory. If you need assistance with Form 8288B preparation, click here, Form 8288B Service.

What if the US Escrow agent/attorney assisting with the sale cannot wait for ITIN or Withholding exemption approval and proceed with FIRPTA tax remittance and issue me Form 8288 and Form 8288A. Can I claim the FIRPTA tax withholding from IRS via a refund claim?

“The Good news is YES, YOU CAN apply for reclaim within four years of sale by applying for ITIN and filing US Nonresident Alien Tax filing.”

In this scenario, you have two options.

OPTION – 1 (If the sale happened in the current year, for example, 2021)

Then start with the ITIN application process with passport certified by IRS approved agents who can assist with all the relevant paperwork checks and supporting documents preview. With this option, you get the ITIN number in 6 to 8 weeks first, and then later next year in 2022, when IRS releases 2020 US tax forms, The seller can file the US Nonresident tax return 1040NR along with Form 8288A. However, under this route, the refund claim process could take around 18 months from the date of sale.

OPTION – 2 (If the sale happened in the prior year, for example, 2020 or earlier)

Then it’s highly recommended to submit an ITIN application along with a 1040NR US tax return and 8288A withholding process. This way, you save time on the ITIN application and tax refund processing time. The FIRPTA tax reclaims refund processing time between 6 to 9 months.

The video below explains the FIRPTA Process for your easy reference.

If you are in the process of selling a USA property and need assistance in completing form 8288-B (If your US Selling agent unable to assist) or if you are required to file Form W-7 for an ITIN application at closing or at a later stage to reclaim the FIRPTA tax. Our team can assist. We are one of IRS approved Certified Acceptance Agents (CAA) with many years of experience dealing with ITIN office and FIRPTA work.

Please visit our website for FAQ related to ITIN and US Tax Assistance.

Visit our website WWW.TAXANDACCOUNTINGHUB.COM

OR WWW.ITINCAA.COM for more ITIN/US tax based FAQ.

Email Us: [email protected].

Call us on: L: +442082211154, M: +447914393183.

For overseas clients. We can arrange for a skype interview if the documents are sent to one of our representative teams.

Our Skype ID is: TAH2108